Cash pooling in the context of Swedish corporate law and group financing structures

Cash pooling is often presented as a straightforward treasury tool for centralising liquidity and reducing funding costs. While the commercial advantages can be significant, a Swedish group structure that may include acquisition financing, minority ownership, guarantees or external security also requires careful attention to a broader set of corporate law and financing issues. This article examines those issues by distinguishing between physical and notional cash pooling and considering how those structures interact with Swedish rules on value transfers, prohibited loans and capital maintenance. It also considers the practical implications for guarantees, collateral packages and enforcement within group financing structures.

Cash pooling is widely used by corporate groups to centralise liquidity, reduce external funding costs and improve day‑to‑day treasury management. By offsetting surplus cash against deficit positions across group companies, it can reduce idle balances and lessen reliance on external debt. Operationally, it is often treated as a technical treasury arrangement, implemented at group level and run by finance teams with limited input from legal advisers. The commercial upside is many times apparent.

From a legal perspective, however, cash pooling is rarely neutral. Once it sits within a group that also has acquisition debt, minority shareholders, external security packages or upstream cash flows, it becomes part of a broader legal and financial structure. Questions then arise about the legal characterisation of intragroup exposures, the limits imposed by the Swedish Companies Act on value transfers and prohibited loans, and the interaction between cash pooling mechanics and collateral and enforcement strategies. Although those issues may initially appear theoretical, they tend to emerge as concrete legal and structuring constraints in stress scenarios, refinancings, enforcement situations or shareholder disputes, often when structural flexibility has already been lost.

This article examines cash pooling from a Swedish law perspective and identifies the main legal issues that arise when cash pooling is introduced into an existing or proposed group financing structure. It first distinguishes between physical and notional cash pooling, then considers the implications under Chapters 17 and 21 of the Swedish Companies Act, and finally addresses the consequences for security, enforcement and broader group leverage. The focus throughout is on how cash pooling interacts with corporate law limits, ownership structures and security arrangements, rather than on operational or accounting considerations.

Physical and Notional Cash Pooling from a Legal Perspective

The starting point for the legal analysis is the distinction between physical and notional cash pooling. Although the economic objective may be similar in both structures, the legal consequences differ significantly.

In a physical cash pool, actual transfers of funds take place between participating accounts and a master account, typically through daily or periodic sweeps. Positive balances are transferred to the master account and negative balances are covered by transfers from the master account. From a legal perspective, this structure gives rise to intragroup loans between the companies participating in the pool. The direction, quantum and duration of these loans depend on daily cash positions, but the legal consequence remains that one group company is lending funds to another.

In a notional cash pool, by contrast, no physical transfers are made. Each company retains its own account and, often, its own credit facilities. Debit and credit balances are notionally aggregated by the bank for interest and utilisation purposes. Because funds are not transferred between group companies, notional pooling does not in itself create intragroup loan relationships. Instead, participants commonly assume broader liability to the cash pool bank, through joint and several liability, cross‑guarantees or similar arrangements.

The distinction is critical under Swedish law. Physical pooling must be analysed through the lens of intragroup lending and its compatibility with Swedish corporate law constraints. Notional pooling, while not creating internal loans, raises distinct issues relating to guarantees, shared liability and the predictability of each participant’s exposure. Treating the two structures as legally interchangeable can lead to misplaced assumptions about risk allocation and compliance.

Value Transfer Constraints under Chapter 17 of the Swedish Companies Act

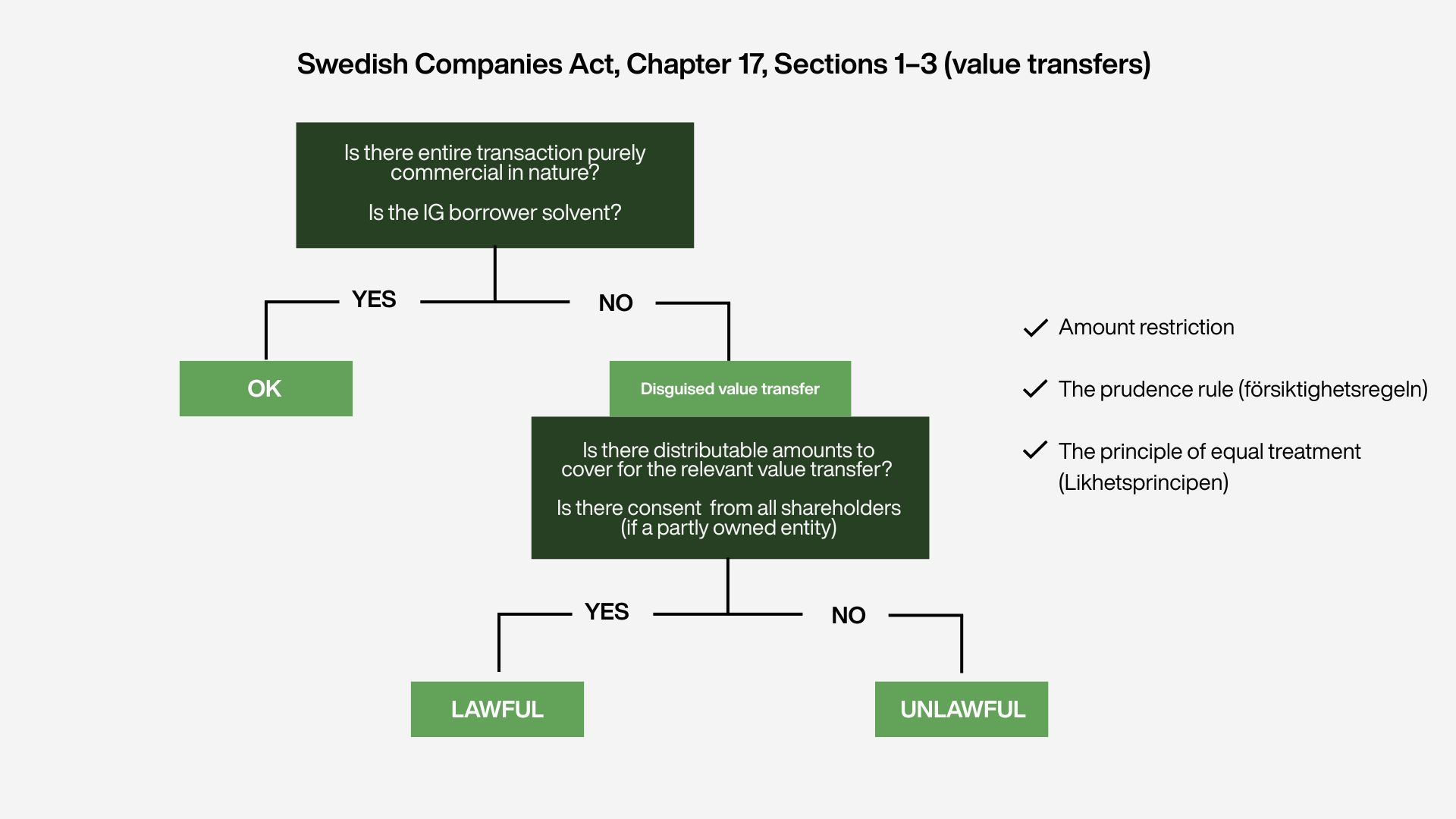

Once the structure has been characterised, the next question is whether the exposures it creates may constitute value transfers under Chapter 17 of the Swedish Companies Act, and if so whether those value transfers may be unlawful.

Under Chapter 17 of the Swedish Companies Act, any transaction that results in a reduction of a company’s assets and that is not of a purely commercial nature for the company may be regarded as a value transfer, even if it is not formally structured as a dividend or similar distribution. This concept of disguised value transfers is of particular importance in group contexts, where transactions may be commercially rational at group level but less clearly justifiable at the level of an individual subsidiary.

In a physical cash pool, value transfer concerns typically arise where a company with surplus cash lends funds to a parent company, a sister company or a non‑wholly owned subsidiary. A key issue is whether the intragroup loan amounts to a value transfer. The question is not whether the group as a whole benefits from the arrangement, because Swedish law does not recognise a general concept of group benefit in this context, but whether the lending company receives adequate consideration and whether the transaction is commercially justified for that entity. The risk becomes more pronounced where loans are advanced to companies with weak credit profiles or limited repayment capacity, or where the lending company is itself partially owned. A risk of reclassification may also arise if the loan terms differ materially from market practice.

In notional cash pools, value transfer issues may arise in a different way. Although no funds are transferred, a company may assume liability for obligations incurred by other group members. The legal and economic value of that exposure can be difficult to quantify, particularly where the structure involves uncapped or fluctuating guarantees. This makes it harder to assess whether the exposure is commercial and whether it can be supported by distributable reserves.

The Swedish Companies Act permits value transfers only to the extent distributable assets are available and the amount restriction and prudence rule are satisfied. These assessments are based on book values rather than market values, which adds a further layer of complexity. In groups with minority shareholders, the principle of equal treatment further limits flexibility. Disguised value transfers involving partially owned subsidiaries may be permissible only with the consent of all shareholders, which makes early structural planning important.

In practice, cash pooling arrangements often include contractual safeguards designed to mitigate these risks. These may include express limitations tied to the value transfer provisions of the Companies Act, solvency representations, market-standard interest rates for intragroup loans, caps on intragroup exposures linked to distributable reserves, and mechanisms to exclude non-wholly owned, insolvent or financially distressed entities from the pool. While such measures do not eliminate legal risk entirely, they can materially reduce the likelihood of breach and show an intention to operate within the statutory framework.

Figure 1. A simplified decision tree for assessing disguised value transfers under the Swedish Companies Act.

Restitution and Liability Considerations

The consequences of an unlawful value transfer extend beyond questions of validity. Chapter 17 of the Companies Act contains restitution and deficiency coverage provisions that can give rise to repayment obligations and personal liability in certain circumstances.

If a value transfer is unlawful, the transaction may be invalid and the recipient may be required to repay what was received if it realised, or ought to have realised, that the transaction constituted a value transfer. The threshold of bad faith is not particularly high. It concerns awareness that the transaction was a value transfer, rather than awareness of the precise legal breach or the fact that the value transfer was unlawful. In cash pooling scenarios, this may become relevant where funds are upstreamed or written off through mechanisms such as netting or set‑off, particularly in distressed situations.

If restitution cannot be made in full, secondary liability may arise for those who participated in the decision or execution of the value transfer. While liability generally requires intent or gross negligence, this does not in itself imply any extensive duty to conduct a full review of the transaction’s legality. The risk may nevertheless increase once a structure enters financial difficulty and it becomes harder to demonstrate corporate benefit or the availability of distributable assets. For banks and advisers involved in designing or operating cash pools, this underlines the importance of identifying and addressing corporate law issues early, rather than assuming they will be solved by practical performance over time.

Prohibited Loans and Financial Assistance under Chapter 21 of the Swedish Companies Act

Even where a cash pooling arrangement can be managed within the value transfer regime, a separate set of issues arises under Chapter 21 of the Swedish Companies Act, which restricts certain loans and guarantees.

As a starting point, Swedish limited companies are prohibited from providing loans or security to a defined circle of related parties, including certain shareholders, board members and related entities. While there are important exceptions, including for group companies within the EEA, these restrictions can become relevant in cross‑border groups with non‑EEA ownership, minority shareholdings or complex holding structures.

Cash pooling may inadvertently involve prohibited lending if funds are advanced to entities within the restricted circle or if guarantees are structured without sufficient regard to ownership and control. Guidance in published case law and legal literature remains limited. However, legal commentary and certain decisions by the Swedish Tax Agency (Sw. Skatteverket) indicate that cash pooling arrangements may fall within the commercial loan exception in Section 21:2 of the Companies Act, provided the transaction is commercially justified for the lender and supports the borrower’s existing business. This may be particularly important where the top account holder is outside the EEA and the ordinary group company exemption is unavailable.

Financial assistance restrictions add another layer of complexity in acquisition financing contexts. Where a target group participates in a cash pool, there is a risk that funds borrowed within the pool could be used to service acquisition debt, potentially triggering the prohibition on financial assistance. Common mitigants include excluding bid vehicles from the pool, limiting the permitted use of funds or deferring the target group’s accession to the cash pool following closing. As with value transfer issues, these points are best addressed at the structuring stage rather than retrospectively.

The consequences of a breach of Chapter 21 should also be kept in view. If a company provides a loan in breach of the chapter, the recipient is in principle required to repay what it has received. If a guarantee or other security is provided unlawfully, the legal act may be unenforceable against the company where the beneficiary knew, or ought to have known, of the breach. Depending on the circumstances, a breach may also expose those involved to damages claims under Chapter 29 and, in more serious cases, criminal sanctions under Chapter 30.

Cash Pooling, Security and Enforcement

The analysis then moves from corporate law constraints to financing structure. Cash pooling is often implemented alongside external bank financing in which share pledges, account pledges and intragroup receivable pledges form part of the security package. In these situations, cash pooling can materially affect the value of the collateral and the viability of the enforcement strategy.

A recurring concept in leveraged finance is single point enforcement, under which enforcement is intended to occur at a defined structural level, typically the top holding company. To create a robust single point of enforcement, shares in the relevant enforcement entity, together with any downstream loans to that entity, are typically pledged, those pledges are fully perfected, and upstream loans from that entity are preferably eliminated. Cash pooling can undermine this approach by altering value flows and creating shifting intragroup exposures that complicate enforcement. Physical pooling is particularly difficult to reconcile with this structure because it presupposes the free movement of funds, while the loans supporting the enforcement model may need to remain fully perfected; it also generates upstream loans that may dilute the value of pledged shares or disrupt clean enforcement pathways. Notional pooling may likewise create guarantee obligations between participants that complicate enforcement, particularly if entities sold to new owners would otherwise remain liable for obligations of former holding companies. Lenders in leveraged financings therefore often require entities above the single point of enforcement to be excluded from the cash pool in order to simplify a potential enforcement process.

Pledging bank accounts within a cash pool presents additional challenges under Swedish law. Typically, cash pool accounts other than the master account are not real accounts but merely addresses, so pledging them is generally not considered technically possible. In addition, perfection measures such as blocking can paralyse the cash pool and effectively prevent the group from operating. Similarly, pledging intragroup loans arising within a cash pool is often impractical, because those loans are temporary, fluctuating and inconsistent with the free flow of funds that cash pooling presupposes.

These tensions highlight the need to consider cash pooling and security structures together. In some cases, it may be appropriate to exclude longer‑term structural intragroup loans from the pool, impose clean‑down requirements or cap balances in order to preserve enforceability. In other cases, it may be preferable to accept reduced collateral coverage in exchange for operational flexibility. The key point is to identify these trade‑offs consciously, rather than letting them emerge inadvertently.

Intragroup and Upstream Loans as a Hidden Layer of Leverage

Physical cash pooling inevitably creates a layer of intragroup debt that may not be immediately visible in a standard financing analysis. These upstream and cross‑stream loans can be sizable and may become structurally significant over time. In some enforcement or restructuring scenarios, their presence or absence can determine how efficiently value can be captured.

From a Swedish law perspective, upstream loans are particularly sensitive because of the combined effect of value transfer rules, prohibited loan restrictions and enforcement mechanics. While upstreaming is often necessary to service external debt, especially where operating subsidiaries generate most of the cash flow, it must be carefully calibrated. One pragmatic approach may be to limit upstream exposures to an amount corresponding to distributable reserves, thereby aligning liquidity management with statutory constraints.

Concluding Remarks

Cash pooling is an effective and widely used treasury tool, but it does not operate in a legal vacuum. Under Swedish law, it intersects with capital maintenance rules, value transfer rules and prohibited lending restrictions, as well as with the practical realities of security and enforcement in leveraged structures. Physical and notional pooling give rise to different legal exposures, and neither can be assessed solely by reference to group‑level benefits.

A robust cash pooling structure typically combines careful selection of participants, contractual limitations reflecting statutory constraints, mechanisms to manage solvency and distribution capacity, and deliberate alignment with the group’s financing and collateral architecture. When these elements are addressed coherently at the outset, cash pooling can improve liquidity management without undermining legal compliance or enforcement outcomes. If they are overlooked, the cash pool may instead become a source of friction or risk precisely when flexibility is most needed.